Novated Lease in Australia – Benefits, Drawbacks & Tax Savings Explained (2026 Guide)

Table of Contents

ToggleWith the cost of living continuing to pressure household budgets across Australia, more employees are asking their HR departments and accountants the same question:

Is a novated lease worth considering?

The short answer is that it depends on your income, your vehicle choice, and how long you plan to stay with your employer. The detailed answer requires understanding how novated leases work, who benefits the most, and where the real risks are.

In 2026, the novated lease landscape in Australia has changed a lot due to the federal government’s decision to extend the Fringe Benefits Tax exemption for eligible electric vehicles. This makes EVs under a novated lease one of the most tax-efficient ways to drive a new car in Australia.

For Australians comparing car finance options in 2026, weighing novated lease arrangements against car loans and cash purchases, the ability to reduce tax through a car lease has become a key factor.

This is especially true for employees in the 32.5% and 37% marginal tax brackets. At the same time, higher interest rates and stricter borrowing conditions have affected the financial choices for many Australians.

At AMA Accountants, our Certified Public Accountants and registered tax agents assist clients in Adelaide, Melbourne, Sydney, Perth, Canberra, Darwin, and Tasmania with understanding the total costs of a novated lease.

We help them figure out how much they will save before they sign any documents. This guide provides all the information you need to make a smart choice.

What Is a Novated Lease?

A novated lease is a three-way car financing arrangement between you (the employee), your employer, and the finance company. Under this structure, your employer takes on the obligation of making lease repayments on your behalf deducting the lease costs from your salary before income tax is applied.

This process is commonly known as salary packaging a car in Australia, or salary sacrifice. It is one of the most widely used forms of car finance in Australia for employees seeking to reduce their tax liability through a structured arrangement approved by the ATO.

Because the lease payments come out of your pre-tax income, your taxable income is reduced that means you pay less income tax each pay cycle. The vehicle remains the property of the finance company during the lease term (typically two to five years), and at the end of the term you can pay a lump sum residual value to own the car outright, refinance the residual, or hand the car back and start a new lease.

Novated leases are available to employees of most Australian companies that offer salary packaging benefits. Government employees in South Australia, Victoria, New South Wales, Western Australia, the ACT, Queensland, the Northern Territory, and Tasmania have historically had access to some of the broadest salary packaging arrangements in the country, given favourable FBT treatment for public sector employees.

How It Works — A Simple Example:

Employee income: $100,000 per year | Novated lease cost: $12,000 per year (pre-tax)

Taxable income after salary sacrifice: $88,000

Estimated annual income tax saving: approximately $3,900 per year (based on 32.5% marginal rate)

Note: Actual savings depend on your marginal tax rate, FBT applicability, vehicle type, and employer’s salary packaging arrangement. Speak to a registered tax agent before proceeding.

Key Benefits of a Novated Lease in Australia (2026)

Tax Savings Through Pre-Tax Salary Deductions

The most significant financial benefit of a novated lease is the reduction in your taxable income. Because lease repayments are deducted from your gross salary before PAYG withholding is calculated, you effectively pay for your car with pre-tax dollars. The higher your marginal tax rate, the greater the benefit.

For a taxpayer earning $120,000 in Sydney, Melbourne, or Perth — sitting in the 37% marginal tax bracket — salary packaging a $15,000 annual lease cost reduces their tax liability by approximately $5,550 per year. Over a four-year lease, that is a potential saving of more than $22,000 in income tax alone, before any additional benefits are considered.

FBT Exemption for Electric Vehicles — A Game Changer

Since 1 April 2022, the Australian federal government has exempted eligible electric vehicles from Fringe Benefits Tax under a novated lease arrangement — provided the vehicle’s value is below the luxury car tax threshold ($91,387 for 2025-26). This is one of the most significant tax concessions available to Australian employees in recent years.

Fringe Benefits Tax would ordinarily apply to employer-provided vehicles and represents a substantial cost under a standard novated lease arrangement. For most petrol or diesel vehicles, FBT is calculated at 20% of the car’s base value per year — reducing the net tax benefit of the lease considerably. For eligible EVs, this cost is completely eliminated.

The EV novated lease tax benefits available in 2026 are substantial, and the vehicle range has expanded considerably. FBT-exempt models popular under a novated lease in Australia include the Tesla Model 3, BYD Atto 3, BYD Atto 2, Hyundai Ioniq 6, Kia EV6, and MG ZS EV. The BYD Atto 2, with its competitive entry price well below the luxury car tax threshold, has become one of the most cost-effective EV novated lease options for employees in Adelaide, Melbourne, and Perth who want to reduce tax in Australia through a car lease while keeping their total lease commitment manageable.

Plug-in hybrid electric vehicles (PHEVs) were also eligible until 31 March 2025, when the exemption was removed for new PHEV agreements. If you are considering any eligible EV in Adelaide, Melbourne, Sydney, Perth, Canberra, Darwin, or Hobart, Tasmania, a novated lease structured as salary packaging a car in Australia is almost certainly the most tax-efficient way to finance it.

GST Savings and All-In-One Running Costs

When a novated lease provider acquires a vehicle on your behalf, they purchase it as a business transaction — meaning they can claim back the GST on the purchase price. This GST saving is typically passed through to you, effectively reducing the vehicle’s cost by approximately 9% before the lease even begins.

Most novated lease packages also bundle all running costs — fuel or charging, comprehensive insurance, registration, tyres, and scheduled servicing — into a single fortnightly deduction. This simplifies your personal cash flow and ensures all running costs benefit from the pre-tax treatment where allowable under ATO rules. It also removes the inconvenience of managing multiple car-related expenses separately.

Drawbacks of a Novated Lease — What You Need to Know

A novated lease is not the right solution for everyone. Before committing to a three to five-year arrangement, every Australian employee should understand the following risks and limitations clearly.

Key Drawbacks — Understand These Before You Sign:

- • Limited savings at lower income levels: If your taxable income is below $45,000 per year, your marginal tax rate of 19% means the pre-tax savings are modest. The tax benefit narrows considerably the lower your income. For lower-income earners in Adelaide, Darwin, or Tasmania, a standard car loan may be more cost-effective.

- • You do not own the car: The vehicle belongs to the finance company throughout the lease. You only gain ownership if you pay the residual value at the end of the term — which can be a substantial lump sum, often 28% to 46% of the original purchase price depending on the lease term.

- • Job change or early termination: If you change employers mid-lease, you must either take over the lease repayments from your own post-tax income or pay an early termination fee, which can be thousands of dollars. This is one of the most frequently overlooked risks of novated leases, particularly in industries with high staff turnover across Sydney, Melbourne, and Perth.

- • Higher total cost versus a loan or cash purchase: When you factor in lease interest rates, establishment fees, and the running cost margin built into novated lease packages, the total amount paid over the life of the arrangement often exceeds what you would pay through a standard car loan or cash purchase — particularly for petrol vehicles where no FBT exemption applies.

- • Reduced borrowing capacity: Because a novated lease deduction reduces your take-home pay, mortgage lenders view it as a financial commitment and reduce your assessed borrowing capacity accordingly. If you are planning to apply for a home loan in Adelaide, Melbourne, Sydney, or Perth within the lease term, speak to AMA Accountants before entering a novated lease arrangement.

- • Running cost estimates may exceed actual usage: Novated lease providers estimate fuel, servicing, and tyre costs in advance. If you drive less than the agreed kilometres, you will have overpaid into the running cost component. Any credit is typically returned at year-end but represents an interest-free loan to the provider in the interim.

- • Policy risk on FBT exemptions: The EV FBT exemption is a government policy that can be changed, limited, or removed at any future federal budget. If you are entering a five-year lease on the basis of the current FBT exemption, you should understand that future policy changes could affect the economics of your arrangement mid-lease.

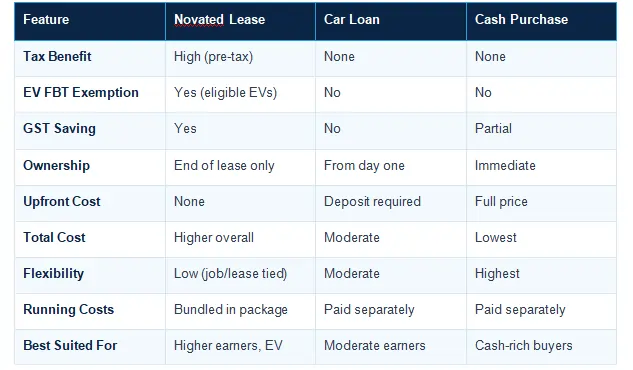

Novated Lease vs Car Loan vs Cash Purchase — Full Comparison

Understanding where a novated lease sits relative to the alternatives is critical before making a decision. When completing a car finance comparison in Australia — particularly between a novated lease, a standard car loan, and a cash purchase — the differences in tax treatment, total cost, and ownership structure are significant. The table below summarises the key differences across all three options to help you decide which form of car finance in Australia suits your situation best.

The table makes it clear that a novated lease delivers its strongest advantage for higher-income earners driving eligible EVs, where the combination of pre-tax savings and FBT exemption is at its most powerful. For petrol vehicles and lower-income earners, a car loan or cash purchase will often represent a lower total cost despite the absence of tax benefits.

Is a Novated Lease Worth It in 2026?

A novated lease is most likely to be worth it if all of the following conditions apply to your situation:

- Your taxable income is $80,000 or above: placing you in the 32.5% or 37% marginal tax bracket where pre-tax savings are material

- You are selecting an eligible electric vehicle: to take full advantage of the current FBT exemption before any future policy changes

- You are stable in your current employment: with no near-term plans to change jobs within the lease term

- You do not plan to apply for a mortgage soon: or have already secured your home loan before entering the arrangement

- You are comfortable not owning the vehicle: and understand the residual payment required at the end of the lease

A novated lease is less likely to be worth it if your income is below $60,000, you drive very few kilometres per year, you are likely to change jobs, or you are planning a significant loan application in the near future. In these scenarios, the simplicity and lower total cost of a car loan or cash purchase may be more appropriate.

AMA Accountants Recommendation:

Never enter a novated lease arrangement without first having a registered tax agent and CPA calculate your actual after-tax saving based on your personal income, vehicle choice, and employment situation.

Generic online calculators use assumptions that may not reflect your real marginal rate, FBT position, or employer’s salary packaging rules. The difference between a well-structured novated lease and a poorly considered one can be thousands of dollars.

Talk to a CPA Before You Commit

A novated lease can be an excellent financial tool for the right person in the right situation — particularly in 2026, where the EV FBT exemption makes electric vehicles under a novated lease one of the most genuinely tax-efficient benefits available to Australian employees. But it is not a one-size-fits-all solution, and the risks of entering a poorly structured arrangement are real.

At AMA Accountants, our Certified Public Accountants and registered tax agents provide personalised novated lease assessments for employees across Adelaide, Melbourne, Sydney, Perth, Canberra, Darwin, and Tasmania. We will calculate your actual tax saving, assess the impact on your borrowing capacity, and help you understand whether a novated lease or an alternative financing option represents the better outcome for your individual circumstances.

Get a Personalised Novated Lease Assessment from AMA Accountants

Before you sign a novated lease agreement, let our CPA team run the numbers for your exact income, vehicle, and employment situation. We provide clear, jargon-free advice with no obligation — so you can make a fully informed decision.

Call: 0420 529 890 | Website: www.amaaccountant.com.au

Certified Public Accountants | Registered Tax Agents | Tax Practitioners Board Registered

Serving Adelaide | Melbourne | Sydney | Perth | Canberra | Darwin | Tasmania | Australia-Wide

Authored By Amit Chugh

Partner, CPA & Registered Tax Agent

Your Trusted Accountant for Adelaide, Melbourne, Sydney, Brisbane & Across Australia

Amit Chugh is a Partner at The AMA Accountant and a highly respected CPA & Registered Tax Agent with a proven track record of delivering exceptional accounting and taxation services to individuals, businesses, and corporations across Australia.

With over 25+ of professional experience, Amit has helped thousands of clients streamline their finances, optimise tax returns, and ensure full compliance with Australian Taxation Office (ATO) requirements. His client base spans Melbourne, Brisbane, Sydney, Tasmania, Perth, Adelaide, Darwin, Canberra, and regional hubs including Prospect, Modbury, Mawson Lakes, Woodville, Mount Gambier, Victor Harbor, Whyalla, Port Lincoln, Murray Bridge, Port Augusta, Gawler, and Port Pirie.

Disclaimer

This content is for general informational purposes only and does not constitute financial, tax, legal, or business advice. Outcomes may vary based on individual circumstances, applicable laws, and current regulations, which may change over time.

We recommend seeking personalised advice from a qualified professional before making any decisions. AMA Accountants is a registered provider of accounting and tax services in Australia.